The three documents people in India use for private loans, promissory note, loan agreement, and IOU, are not interchangeable. They have different legal weights, different stamp duty schedules, different limitation periods, and (most importantly) lead to very different outcomes when you have to recover money from a reluctant borrower.

Here's how to pick the right one for your situation.

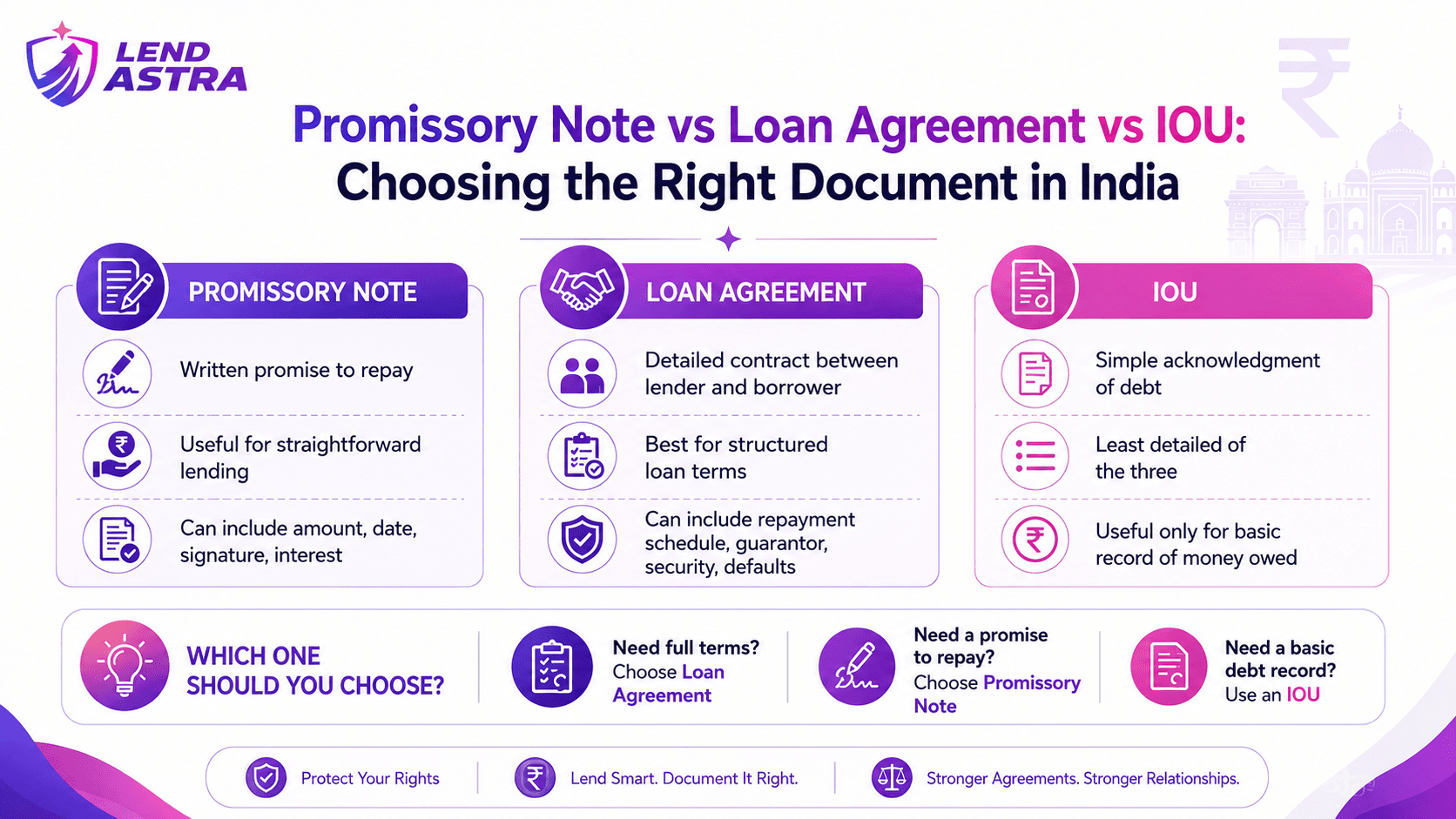

The 30-second decision table

| Your situation | Use this |

|---|---|

| One-shot loan, fixed sum, single repayment date, no instalments | Promissory note |

| Multi-instalment loan, interest, collateral, default terms | Loan agreement |

| Acknowledgment of an already-disbursed amount, no new terms | IOU (weakest, avoid if possible) |

Promissory note, the streamlined civil weapon

A promissory note is governed by Section 4 of the Negotiable Instruments Act, 1881. It's defined as an "instrument in writing... containing an unconditional undertaking, signed by the maker, to pay a certain sum of money only to, or to the order of, a certain person, or to the bearer".

Three magic words: unconditional, certain sum, signed.

What a valid promissory note looks like:

On demand (or On 15th August 2026), I, Rajesh Malhotra, S/o Mahesh Malhotra, residing at Flat 302, Vashi Sector 17, Navi Mumbai, 400703, hereby unconditionally promise to pay Smt Priya Sharma, residing at Flat 805, Belapur Sector 11, Navi Mumbai, 400614, the sum of ₹3,00,000 (Rupees Three Lakh only) with interest at 12% per annum computed from 20th May 2026.

Signed at Navi Mumbai on this 20th day of May 2026.

[Stamp of value ₹600] [Signature] [Two witness signatures]

Stamp duty for a promissory note (Maharashtra, 2026): ₹0.20 per ₹100 of the sum, so ₹600 stamp on a ₹3 lakh note.

Why lenders love pro notes:

- Order 37 CPC summary suit. A pro note debt qualifies for the summary procedure under Order 37 of the Civil Procedure Code. The defendant must seek leave to defend within 10 days; if no defence is permitted, decree is issued without trial. Speed: 60–120 days vs 18–36 months for a regular civil suit.

- Section 138 NI Act crossover. If the borrower issues a cheque against the pro note and it bounces, criminal proceedings begin.

- Limitation period. Three years from the date payment is demanded (or from the date of execution if payable on demand).

Why pro notes don't fit everything:

- They can't contain elaborate clauses (collateral, prepayment penalties, multi-tranche disbursal). They're stripped down by design.

- "Certain sum" means a single figure, instalment schedules don't fit naturally.

- Once a pro note is paid, it's typically destroyed or returned (it's a negotiable instrument).

Loan agreement, the flexible contract

A loan agreement is governed by the Indian Contract Act, 1872. Unlike a pro note, it's a full contract that can contain whatever lawful clauses both parties agree to.

A standard loan agreement contains:

- Parties, full identification of lender and borrower.

- Principal, the amount loaned, with disbursal mechanism (cheque / NEFT / UPI).

- Interest, rate, type (simple / compound / flat / reducing), accrual frequency.

- Tenure & repayment schedule, instalment table with dates.

- Default clause, penalty interest, grace period, what triggers default.

- Collateral / security, if any, with valuation and registration details.

- Prepayment, allowed or not, penalty if any.

- Jurisdiction, which civil court has jurisdiction in case of dispute.

- Witness signatures, minimum two adult witnesses.

Stamp duty for a loan agreement in Maharashtra (Article 5(h)(A) of Schedule I):

| Loan amount | Stamp duty |

|---|---|

| Up to ₹50,000 | ₹100 |

| ₹50,001–₹2,50,000 | ₹200 |

| ₹2,50,001–₹5,00,000 | ₹500 |

| ₹5,00,001–₹10,00,000 | ₹1,000 |

| Above ₹10,00,000 | ₹2,000 (capped) |

Limitation period. Three years from when the cause of action arises, usually the date of default on a specific instalment.

When the loan agreement wins:

- You're charging interest with a complex schedule.

- The loan has collateral (vehicle, property, gold).

- Multi-tranche disbursal is involved.

- You want to encode default penalties, prepayment terms, or jurisdiction clauses.

- The amount is significant (₹5 lakh+).

IOU, what it is, why to avoid it

"IOU" stands for "I Owe You". In Indian legal practice, an IOU is a bare acknowledgment of debt, a written statement that money is owed, without an unconditional promise to repay.

A typical IOU:

I, Rajesh Malhotra, acknowledge that I have received ₹3,00,000 from Priya Sharma on 20th May 2026.

[Signature]

That's it. No promise to repay, no date, no interest, no jurisdiction.

Why this is legally weak:

- It's not a negotiable instrument (no NI Act protection, no Section 138 cheque-bounce path).

- It's not a contract in the full sense (no consideration, no promise, just acknowledgment).

- It can be used as evidence that the money was given, but it doesn't independently create a promise to repay.

- Recovery requires a separate civil suit under "money had and received", slower, more uncertain.

Use an IOU only when: You've already disbursed money informally and the borrower won't sign anything stronger today. Use it as a bridge to a proper document later.

Limitation Act periods, the three-year killer

The Limitation Act, 1963 sets time limits on enforcement. Miss the window and your right to recover dies.

| Document | Limitation period | Counted from |

|---|---|---|

| Promissory note (on demand) | 3 years | Date of execution |

| Promissory note (specific date) | 3 years | The specific date |

| Loan agreement | 3 years | Date of default on the relevant instalment |

| IOU | 3 years | Date of acknowledgment (treated as debt acknowledgment under Section 18) |

| Cheque issued and dishonoured | 3 years | Date of dishonour |

| Mortgaged loan (registered) | 12 years | Date the principal becomes due |

The trick. A fresh acknowledgment in writing, even a WhatsApp message saying "I'll pay you back next month", restarts the limitation clock under Section 18 of the Limitation Act. Keep a running paper trail; never let the three years lapse silently.

Recovery process for each document

Promissory note → Order 37 CPC summary suit. File in the appropriate civil court within 3 years. The court issues a summons to the defendant; the defendant has 10 days to apply for leave to defend. If leave is refused (because there's no triable issue), decree is passed. Typical timeline: 4–8 months.

Loan agreement → Regular civil suit. File in the civil court of appropriate jurisdiction. Court issues summons, defendant files written statement, evidence is recorded, arguments heard, judgment delivered. Typical timeline: 18–36 months. Can be accelerated if the agreement contains an arbitration clause.

IOU → Money suit under "money had and received". Same court process as loan agreement, but with a weaker base, the burden of proving the loan terms (interest, repayment date) falls heavily on you. Typical timeline: 24–48 months.

Three steps to pick the right document right now

- Is the loan a single lump sum repayable in one shot? → Promissory note.

- Are there instalments, interest schedules, or collateral? → Loan agreement.

- Have you already given the money and need a paper trail today? → IOU as a stopgap, then upgrade to a pro note or agreement within 30 days.

Whichever you pick, get it stamped at the value mandated by your state's Schedule I. An unstamped document is admissible only after payment of duty plus penalty, and the penalty in Maharashtra can be up to ten times the duty.

Pick the right document at the start; it's the lowest-effort, highest-impact decision you'll make on the entire loan.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ENotarisation%2C%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERegistration%2C%20and%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EE-Stamping%3A%20When%20Your%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ERenewing%20or%20Extending%20a%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELoan%3A%20Documenting%20a%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERollover%20Cleanly%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)