The single most valuable document in personal lending is also the simplest: a one-page agreement that takes ten minutes to write. Yet most loans between friends and family have nothing on paper, not because people do not want to, but because they imagine documentation means lawyers, jargon, and cost. It does not. A clear, plain-language page is enough, and you can write it yourself today.

Here is exactly what goes on it, and why each line matters.

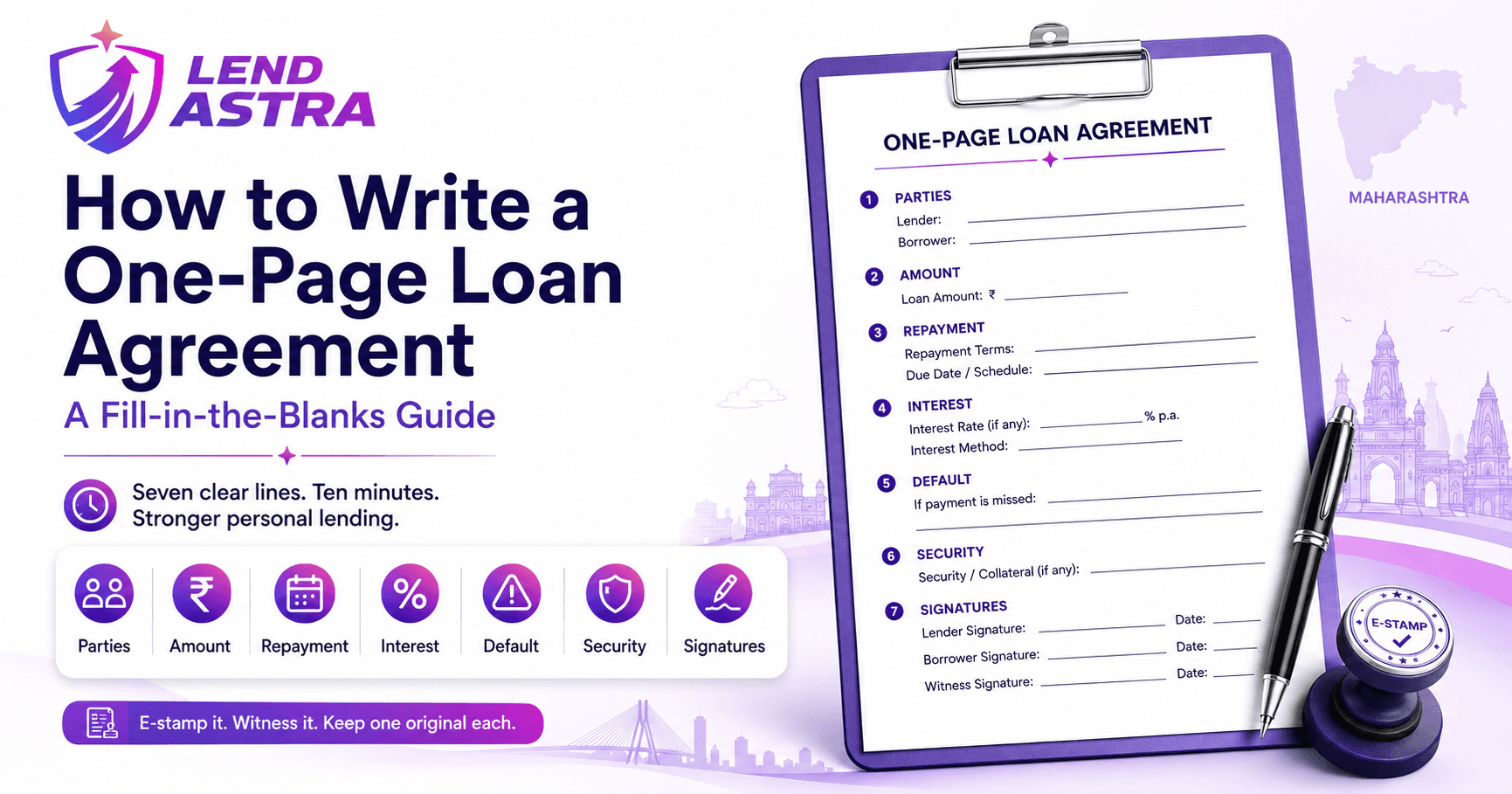

The seven lines that make it valid

A personal loan agreement does not need to be long. It needs to be clear, and it needs seven things.

One, the parties. Full names, with a parent's name and an address for each, so there is no ambiguity about who borrowed from whom.

Two, the amount. The principal in figures and words, "₹2,00,000 (Rupees Two Lakh only)", and the date and mode of disbursal, ideally a bank transfer reference.

Three, the repayment. The exact date or dates by which the money is due, and whether it is a single repayment or instalments.

Four, the interest. The rate, whether it is flat or reducing, and how it is calculated. If the loan is interest-free, say so explicitly.

Five, the default. What happens if repayment is late: any step-up in interest, tied to a clear trigger date.

Six, the security. Any collateral or security cheque, described plainly.

Seven, the signatures. Both parties sign and date, ideally with two witnesses who also sign.

That is the whole document. Everything else is detail.

Stamp it, witness it, keep it

Three small steps turn a written page into a strong one. E-stamp it, a few hundred rupees in Maharashtra, which makes it valid as evidence. Have two witnesses sign. And keep one original each. None of this needs a professional. All of it makes the document hold up if it is ever tested.

The order to write it in

Write the parties first, then the money, then the time, then the terms, then the signatures. Working top-down keeps you from forgetting the boring-but-vital lines, the address, the mode of disbursal, the default trigger, that are precisely the ones disputes hinge on later.

A Navi Mumbai example

In 2026 a Vashi resident lent ₹1,50,000 to a cousin. Rather than a vague WhatsApp promise, she opened a blank page and filled the seven lines in ten minutes: both names and addresses, the amount in figures and words, an NEFT reference, a single repayment date six months out, an 8 percent reducing rate, no security needed for the amount, and both signatures with one witness. She e-stamped it for a few hundred rupees. When the cousin repaid early, there was nothing to discuss, because everything had already been agreed in writing. Ten minutes had removed every future argument.

Your fill-in-the-blanks checklist

- Parties: full names, parent's name, address for each.

- Amount: figures and words, date, and mode of disbursal.

- Repayment: exact date or instalment schedule.

- Interest: rate, flat or reducing, or state interest-free.

- Default: any step-up, tied to a dated trigger.

- Security: collateral or security cheque, if any.

- Signatures: both parties, two witnesses, e-stamped.

The page that prevents the problem

A loan agreement is not bureaucracy. It is a ten-minute conversation, written down, that quietly removes almost every path a loan has to going wrong. You do not need legal language or legal fees. You need seven clear lines, two signatures, and a small e-stamp. Write that page before the money moves, and you turn a risky favour into a clean agreement that protects everyone at the table.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ENotarisation%2C%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERegistration%2C%20and%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EE-Stamping%3A%20When%20Your%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ERenewing%20or%20Extending%20a%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELoan%3A%20Documenting%20a%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERollover%20Cleanly%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)