Why a Written Loan Agreement Is Important Before Giving or Taking Money

Money is often given between friends, relatives, business contacts, employees, customers, or known people based on trust. In many cases, the lender believes the borrower will return the money on time. The borrower also believes that they will repay the amount as promised.

But the problem usually starts later.

The borrower may delay payment. The lender may forget the exact date. The repayment amount may become unclear. Interest, penalty, cheque details, guarantor responsibility, and payment proof may not be properly recorded. Slowly, what started as a simple money transaction can become a stressful dispute.

This is why a written loan agreement is important.

A money lending agreement does not mean that the lender does not trust the borrower. It simply means both parties want clarity. A proper loan agreement helps the lender and borrower record the amount, repayment schedule, terms, responsibility, and proof in one place.

Today, platforms like Lend Astra can make this process simpler by helping users create a digital loan agreement, record borrower and lender details, add guarantor or witness information, and maintain proper documentation.

Why Verbal Promises Are Risky

Many personal loans happen verbally. Someone says, “I will return the money next month,” and the lender agrees. There may be WhatsApp messages, phone calls, or bank transfer screenshots, but these are often incomplete.

A verbal promise can create problems such as:

No clear repayment date

No written interest terms

No proper borrower details

No guarantor responsibility

No record of cheque or security details

No proof that both parties agreed to the same terms

No structured reminder system

When there is no written loan document, both parties may remember the deal differently. The lender may say the loan was for 3 months. The borrower may say it was for 6 months. The lender may say interest was discussed. The borrower may deny it.

A simple written agreement avoids this confusion.

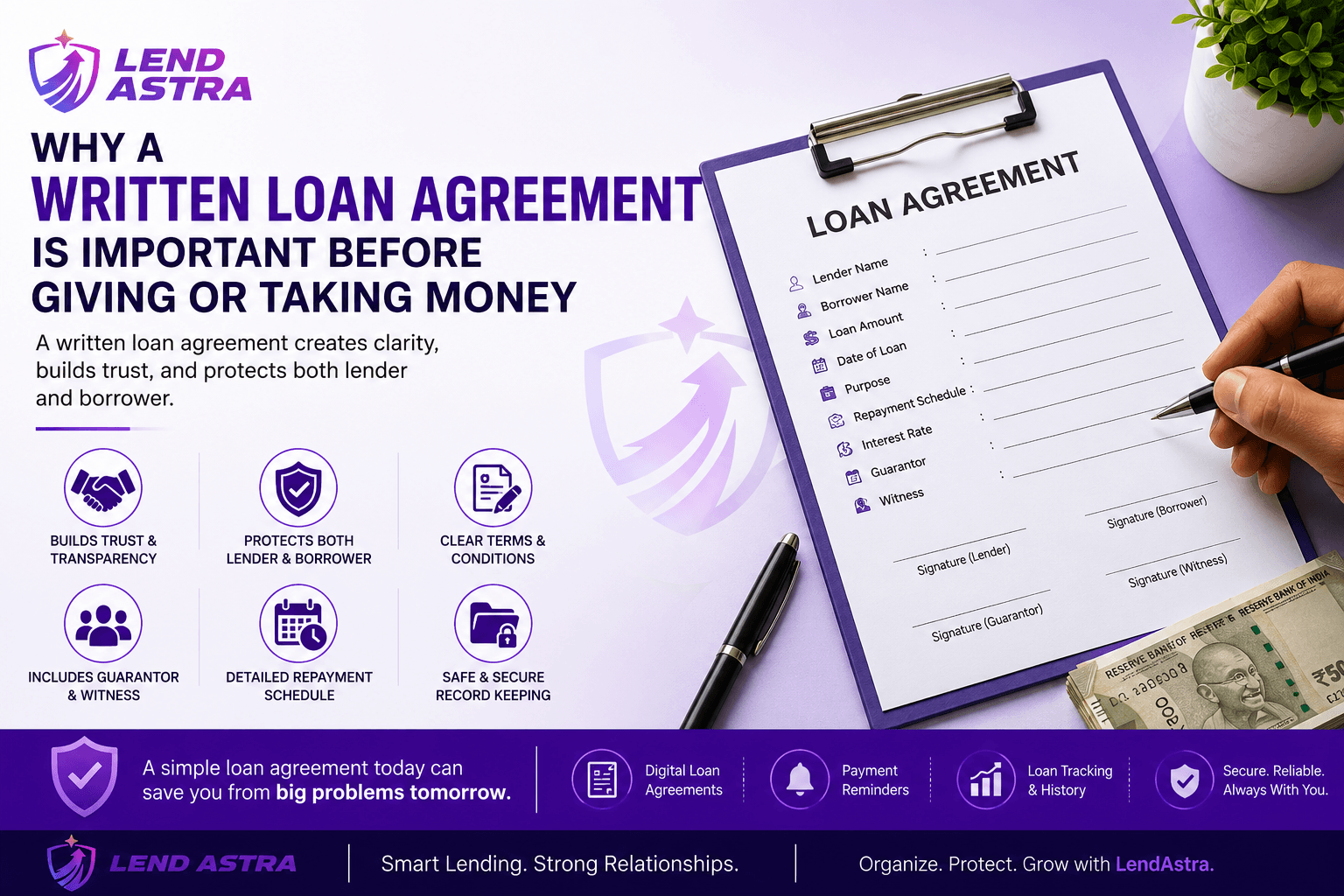

What Is a Money Lending Agreement?

A money lending agreement is a written document between a lender and a borrower. It records the loan amount, repayment date, payment method, interest if applicable, security if any, and the responsibilities of both parties.

A basic personal loan agreement may include:

Name and details of the lender

Name and details of the borrower

Loan amount

Date of loan

Purpose of loan

Repayment schedule

Interest terms, if any

Late payment conditions

Guarantor details, if applicable

Witness details, if applicable

Cheque or security details

Signature or digital acceptance of parties

This document acts as a clear record of the loan transaction.

Why Lenders Should Use a Written Loan Agreement

For a lender, the biggest risk is non-payment or delayed payment. Even if the lender has transferred money through bank, UPI, or cheque, that proof may not clearly explain the purpose of payment.

Was it a loan?

Was it an advance?

Was it a gift?

Was it business payment?

Was it repayment for something else?

A written personal loan agreement clearly states that the amount was given as a loan and must be repaid as per agreed terms.

For lenders, a written agreement helps in:

Creating proper loan proof

Recording borrower identity

Setting repayment expectations

Adding guarantor or witness support

Avoiding future misunderstanding

Keeping all loan records organized

Sending reminders based on due dates

This gives the lender better control and clarity.

Why Borrowers Should Also Prefer a Loan Agreement

Many borrowers feel that a loan agreement only protects the lender. That is not true.

A written loan agreement also protects the borrower.

Without a written agreement, the lender may later claim a different amount, different interest, or a different repayment date. A borrower may repay some amount but may not have a proper record of how much is still pending.

A written agreement helps the borrower by:

Confirming the exact loan amount

Recording the agreed repayment date

Avoiding sudden change in terms

Creating proof of partial payments

Preventing unfair claims

Showing that the borrower accepted clear terms

When both parties know the rules from the beginning, the relationship remains more transparent.

Role of Guarantor and Witness in a Loan Agreement

In many private loans, the lender may ask for a guarantor or witness.

A guarantor is a person who agrees to take responsibility if the borrower fails to repay the loan, depending on the agreed terms. A witness is a person who confirms that the agreement was made between the lender and borrower.

Adding guarantor and witness details can make the loan document stronger and more reliable.

A digital platform like Lend Astra can help record:

Guarantor name

Guarantor contact details

Witness name

Witness contact details

Their acceptance

Their role in the loan transaction

This reduces future denial and confusion.

Importance of a Repayment Schedule

One of the most important parts of any loan agreement is the repayment schedule.

A repayment schedule clearly mentions when and how the borrower will repay the money. It may be a single payment, monthly EMI, weekly payment, partial payment, or custom schedule.

For example:

Full repayment after 30 days

Monthly repayment for 6 months

Interest payment every month and principal at the end

Part payment on fixed dates

When repayment terms are written properly, both lender and borrower can track the loan easily.

A repayment schedule also helps in sending reminders before the due date. This is important because many disputes happen not because of fraud, but because people forget, delay, or avoid difficult conversations.

Why Digital Loan Agreements Are Better Than Manual Paper Agreements

Traditional paper agreements are useful, but they can be difficult to manage. People may lose the paper, forget to take signatures, miss important clauses, or fail to store proof properly.

A digital loan agreement can make the process faster and more organized.

Benefits of digital loan agreements include:

Easy creation of loan document online

Proper borrower and lender details

KYC-based information capture

Digital acceptance by parties

Better record keeping

Easy access from mobile

Payment reminders

Status tracking

Document history

For small personal loans, business loans, family loans, and private lending, this can save time and reduce risk.

Common Mistakes People Make While Giving Money

Many lenders make simple mistakes while giving money. These mistakes can later become expensive.

Common mistakes include:

Giving money without written proof

Not mentioning repayment date

Not collecting borrower identity details

Not adding witness or guarantor

Not saving payment proof

Not recording part payments

Not issuing reminders

Not creating a promissory note or agreement

Depending only on trust

Trust is important, but documentation is equally important.

A loan agreement is not against trust. It protects trust.

How Lend Astra Can Help

Lend Astra can help users create a structured money lending process instead of depending only on verbal promises or scattered WhatsApp messages.

With Lend Astra, the idea is to make private lending more organized by helping users manage:

Loan request

Lender and borrower details

Digital loan agreement

Promissory note

Guarantor and witness details

Repayment schedule

Payment reminders

Document status

Loan history

Proof of acceptance

This can help both parties stay clear from the beginning.

For lenders, it creates better protection.

For borrowers, it creates transparency.

For guarantors and witnesses, it clearly defines their role.

Final Thoughts

Giving money is easy. Recovering money without proper documentation is difficult.

A simple written loan agreement can prevent confusion, protect relationships, and create proper legal proof of the transaction. Whether the loan is between friends, relatives, business contacts, or known people, written terms are always safer than verbal promises.

A money lending agreement, personal loan agreement, repayment schedule, promissory note, and proper borrower details can make the entire process more transparent.

Lend Astra aims to make this process simple, digital, and organized.

Before giving or taking money, create a proper loan agreement. It may take a few minutes today, but it can save months of stress tomorrow.