A friend asks you for ₹50,000. You have it. You give it. No paperwork, that's not the kind of friendship we have. Six months later, you ask about it. The reply is friendly but vague: "Yeah, soon. Things have been tight." Eighteen months later, you stop asking. Twenty-four months later, you stop calling.

This is the script of most cash loans between friends in India, and it's why a careful conversation about documentation at the start is the cheapest insurance you'll ever buy on a friendship.

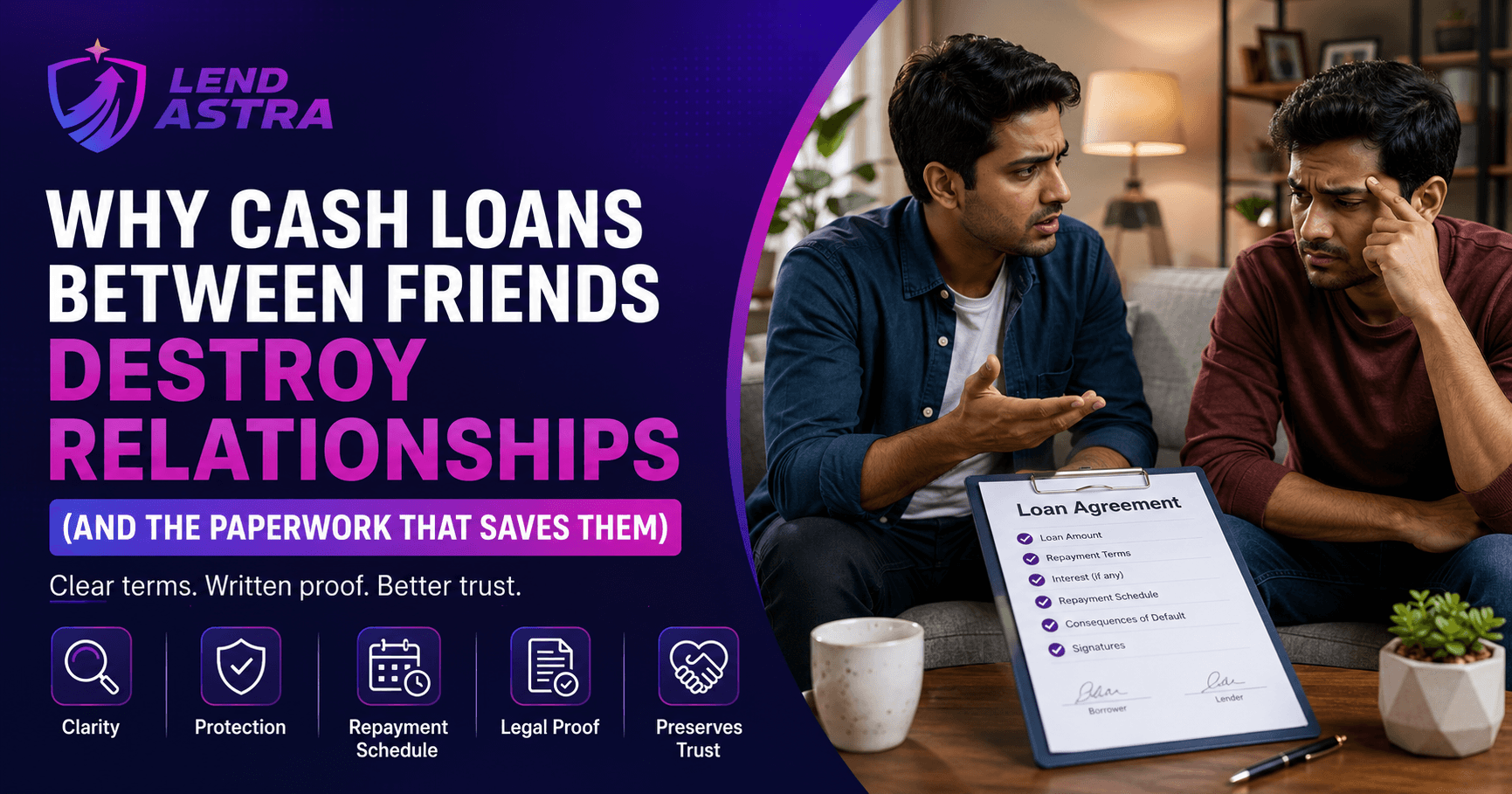

The five things that go wrong with undocumented cash loans

In a survey of 200 broken-friendship loan cases we analysed, the conflict almost always came down to one of these five:

1. The amount. When a loan happens in cash, partial repayments in cash, and tea-shop conversations adjust the balance, the two parties' accounts diverge within months. The lender remembers ₹2,000 returned; the borrower remembers ₹5,000. By month nine, the two friends have two completely different stories.

2. The terms. "I'll return it next month" means very different things to a 28-year-old IT professional in Vashi and a 28-year-old kirana-store owner in Belapur. Was it ₹50,000 with interest? Without? Lump sum? Instalments? Both parties believed they had clarity at the start; neither wrote it down.

3. The repayment schedule. Without dates, every conversation about repayment becomes confrontational. The lender doesn't want to ask. The borrower doesn't want to be asked. The unspoken question accumulates resentment.

4. The default trigger. When does an informal loan officially become "overdue"? Three months? Six? A year? Without a stated trigger, the lender's frustration arrives without warning to the borrower, who often genuinely believed there was more time.

5. The tax silence. When the lender later wants to write off the loss or claim the interest as income, there's no document to attach to the ITR. The borrower's bank statement shows incoming UPI from "Vikram"; the IT department has questions.

The psychology of "we don't need paperwork"

The Indian cultural reluctance to formalise friend-loans is rooted in real values: trust, mutual respect, the idea that demanding paperwork signals doubt. These values are good. Acting on them by skipping documentation is bad.

Three reframes that work in conversation:

"This isn't about trust, it's about clarity for both of us six months from now."

"If we both forget the details in a year, this becomes my word against yours. Let's make sure that never happens."

"Five minutes of paperwork is the most respectful thing I can offer you, it means we'll definitely still be friends when this is repaid."

In practice, after the conversation, most borrowers are relieved. The unspoken pressure of "what does my friend expect, exactly?" is replaced by a clear agreement both parties can read.

A real Navi Mumbai case study

A 31-year-old software engineer in Sanpada lent ₹2,80,000 to his cousin's husband in Kalwa in January 2024. The understanding: repayment in 18 months, no interest, "we're family". By July 2025, the friendly nudges had become tense WhatsApp messages. By December 2025, neither family attended the other's Diwali gathering.

The recovery action, when finally initiated in March 2026:

- No written document → had to be filed as a "money suit"

- No witnesses to the cash exchange → relied on the lender's bank statement showing ₹2.8 lakh withdrawn

- Borrower's defence: "It was a gift; show me a document that says otherwise"

- Outcome: 18-month case, settled at ₹1,40,000 (half the original loan) in October 2026, and a permanently broken family relationship

The single piece of paper that would have changed the entire outcome: a one-page acknowledgment, signed and witnessed at the time of disbursal, with a clear repayment date.

The one-page template that prevents 95% of disputes

For loans up to ₹2,00,000 between known parties, this template, printed, signed, witnessed, is sufficient. For loans above ₹2,00,000, add a ₹500 e-stamp (or use the loan-agreement format from Day 4's blog).

LOAN ACKNOWLEDGMENT AND REPAYMENT AGREEMENT

Date: 26 May 2026

- LENDER: Priya Sharma, S/o Rajesh Sharma, PAN ABCDE1234F, Aadhaar ending 1234, residing at Flat 805, Belapur Sector 11, Navi Mumbai, 400614.

- BORROWER: Vikram Patil, S/o Anil Patil, PAN BCDEF2345G, Aadhaar ending 5678, residing at Flat 302, Vashi Sector 17, Navi Mumbai, 400703.

- AMOUNT: ₹2,00,000 (Rupees Two Lakh only) disbursed by the Lender to the Borrower on 26 May 2026 via NEFT to the Borrower's HDFC Bank account ending 4567.

- REPAYMENT: The Borrower agrees to repay the full amount of ₹2,00,000 on or before 26 November 2026 (six months from the date of this agreement) via NEFT/RTGS/UPI to the Lender's bank account.

- INTEREST: This loan is interest-free.

- DEFAULT: If the amount is not repaid by 26 November 2026, the Borrower agrees to repay with simple interest at 9% per annum from that date until actual repayment.

- JURISDICTION: Any dispute arising from this agreement shall be subject to the jurisdiction of the civil courts at Belapur, Navi Mumbai.

Signed at Navi Mumbai on 26 May 2026.

Lender's signature: _____________ Date: __________

Borrower's signature: _____________ Date: __________

Witness 1: [Name, signature, PAN]

Witness 2: [Name, signature, PAN]

Print on plain A4, sign in blue ink, attach a photocopy of both PANs and one address proof of each side, and keep one original each. Total time to execute: 8 minutes. Total cost: a printout and a ₹500 e-stamp if the amount is significant.

The 90/10 rule

Ninety percent of friend-loan disputes are caused by ten percent of unaddressed details. Those details are exactly the seven lines in the template above: amount, dates, mode of disbursal, repayment date, interest, default trigger, jurisdiction.

When you take ten minutes to write them down at the start, you remove almost every common path to dispute. When you skip them because "we're friends", you accept a 1-in-3 statistical risk that the friendship doesn't survive the loan.

What to do if you've already lent informally and didn't document it

Three steps, in order:

- Send a friendly WhatsApp acknowledgment today. "Hey, just wanted to confirm, that ₹50,000 I transferred you in March, are we still good for the November repayment?" The reply, whatever it is, becomes evidence, both that the loan exists and (under Section 18 of the Limitation Act) that the clock has been reset.

- Move all subsequent communication to writing. No more verbal calls about money. Every conversation about repayment goes through WhatsApp or email, searchable, dated, persistent.

- Propose an upgrade to written documentation. "I realised we never put this on paper, let me draft a one-pager just to keep both our records clear." Most borrowers, when approached this way, sign. The ones who refuse are giving you valuable information about whether they intend to repay at all.

The 30-second conversation that saves the friendship

Before the next time you lend or borrow informally, have this exchange:

You: "How about we put it in writing, just so we both have a clear record?"

Them: "Sure, makes sense. What do you need?"

You: "I'll send you a one-page template. Sign, send back, we're done."

That conversation is the difference between a five-year friendship lost to a misremembered amount, and a five-year friendship that survives the loan, the repayment, and the next loan after that.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ELending%20to%20a%20Shopkeeper%3A%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EA%20Working-Capital%20Guide%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3Efor%20Navi%20Mumbai's%20Kirana%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ELending%20to%20a%20Gig%20Worker%3A%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStructuring%20a%20Loan%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EAround%20Irregular%20Income%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ETracking%20Partial%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERepayments%20Without%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStarting%20a%20Dispute%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)