Every personal loan sits on a quiet question the lender rarely says aloud: what happens if this person simply cannot pay. The answer depends almost entirely on one decision made at the start, whether the loan is secured by something of value or rests purely on a promise.

Most loans between people who know each other are unsecured, and for small, trusted amounts that is fine. But there is a size and a risk beyond which asking for security is not distrust. It is prudence, and done well it protects the friendship as much as the money.

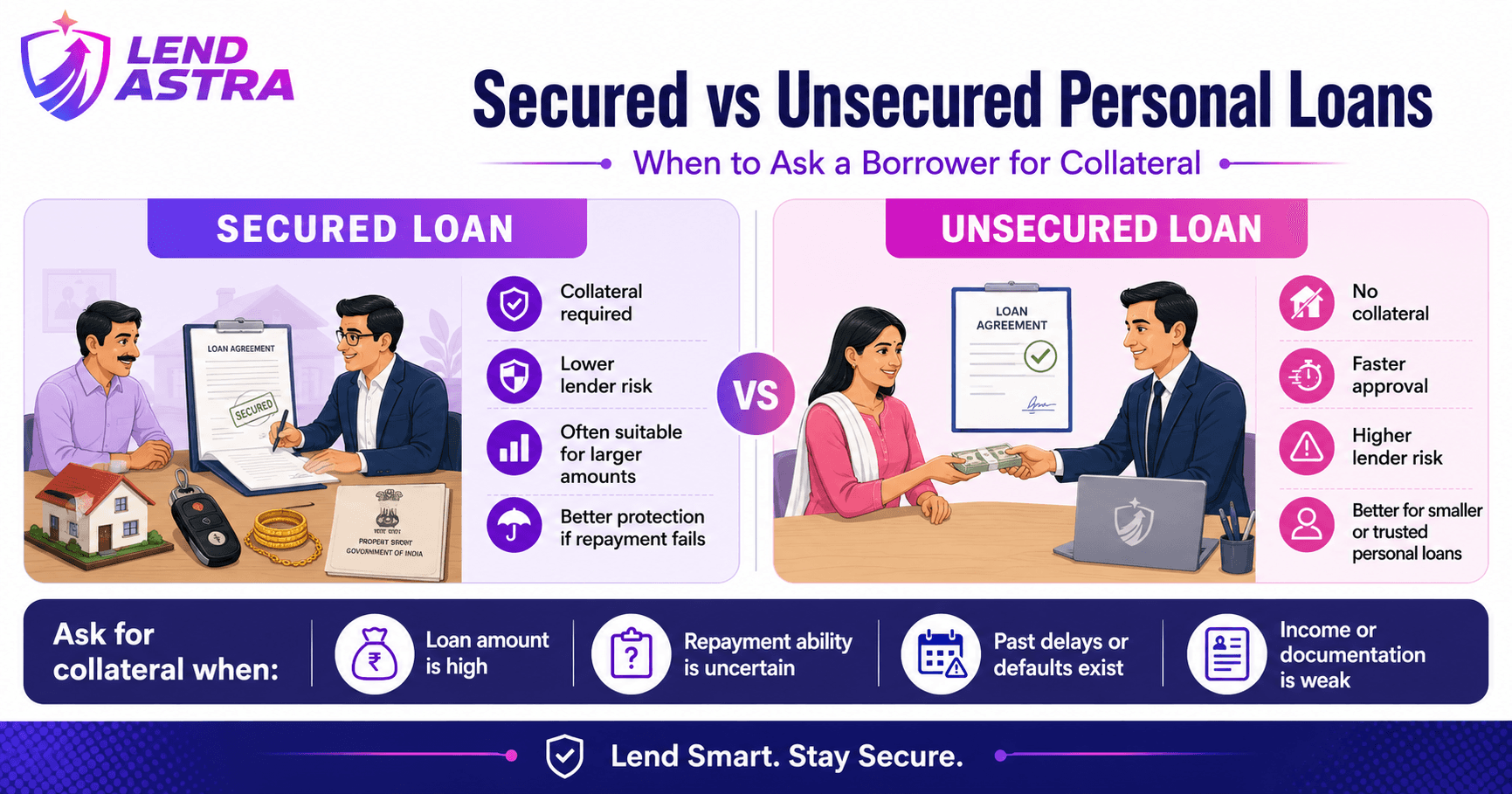

What "secured" actually means

A secured loan is backed by an asset the lender can claim if repayment fails: gold, a fixed deposit, property, a vehicle. An unsecured loan has no such backing. If the borrower defaults, the lender's only route is the slow one, a recovery suit, with no specific asset waiting at the end.

The difference is not academic. Security turns a hopeful recovery into a defined one, and that single fact ripples through everything else about the loan.

When to ask for collateral

You do not need security for ₹20,000 from a colleague repaying next month. You should seriously consider it when three things stack up: the amount is large enough to genuinely hurt to lose, the tenure is long enough for circumstances to change, or the borrower's repayment capacity is uncertain.

A useful rule of thumb: if losing the full amount would change your financial life, ask for security. If it would merely annoy you, an unsecured documented loan is usually enough.

What makes good collateral in India

The best security is liquid, easy to value, and easy to transfer. Gold and a marked lien on a fixed deposit are excellent: clear value, simple to act on. Property is valuable but slow and formal to enforce, and a charge on immovable property must be properly created and often registered. A post-dated or security cheque is not collateral in the asset sense, but it is a powerful enforcement tool under Section 138 of the Negotiable Instruments Act.

Match the security to the loan. For most personal lending, a security cheque plus a clear agreement is the practical sweet spot.

How to ask without offence

The phrasing matters more than the request. Frame security as a way to keep the loan clean and the relationship safe, not as a test of trust. "Let us put a security cheque in place so neither of us has to worry, and we both have a clear record." Most decent borrowers find this reassuring, because it makes the whole thing businesslike rather than emotional.

A Navi Mumbai example

In 2026 a Kharghar lender was asked for ₹5,00,000 by an old friend for an 18-month term. The amount was large and the tenure long, so he asked for security against a friend's gold, with a one-page agreement recording the loan and the lien. Nothing about the friendship changed. When the friend repaid on schedule, the gold was released untouched. The security was never used, but it let the lender say yes to an amount he would otherwise have declined, which is exactly what good collateral does.

A collateral checklist

- Unsecured is fine for small, short, trusted loans.

- Ask for security when the amount would hurt to lose, the tenure is long, or capacity is uncertain.

- Prefer liquid, easy-to-value security: gold, an FD lien, or a security cheque.

- Document the security inside the loan agreement, and register any property charge.

- Frame it as protection for both, not a test of trust.

Security is a yes-enabler, not a no

Collateral is often what makes a fair, larger loan possible at all. It lets a cautious lender extend trust they could not extend on a promise alone, and it gives the borrower access to terms far better than an informal lender would offer. Written into a clear agreement, security protects the money without poisoning the relationship. That is the whole point: not to prepare for betrayal, but to make a generous yes possible.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ELending%20to%20a%20Shopkeeper%3A%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EA%20Working-Capital%20Guide%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3Efor%20Navi%20Mumbai's%20Kirana%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ELending%20to%20a%20Gig%20Worker%3A%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStructuring%20a%20Loan%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EAround%20Irregular%20Income%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ETracking%20Partial%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ERepayments%20Without%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStarting%20a%20Dispute%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)