The Reserve Bank of India regulates organised peer-to-peer lending platforms tightly, and informal lending between individuals barely at all. Most people doing private lending in India don't know which category they're operating in, which means they sometimes follow rules that don't apply and ignore the ones that do.

This is a 2026 cheat-sheet to the actual rule landscape: what RBI cares about, what it doesn't, and where you sit on that map.

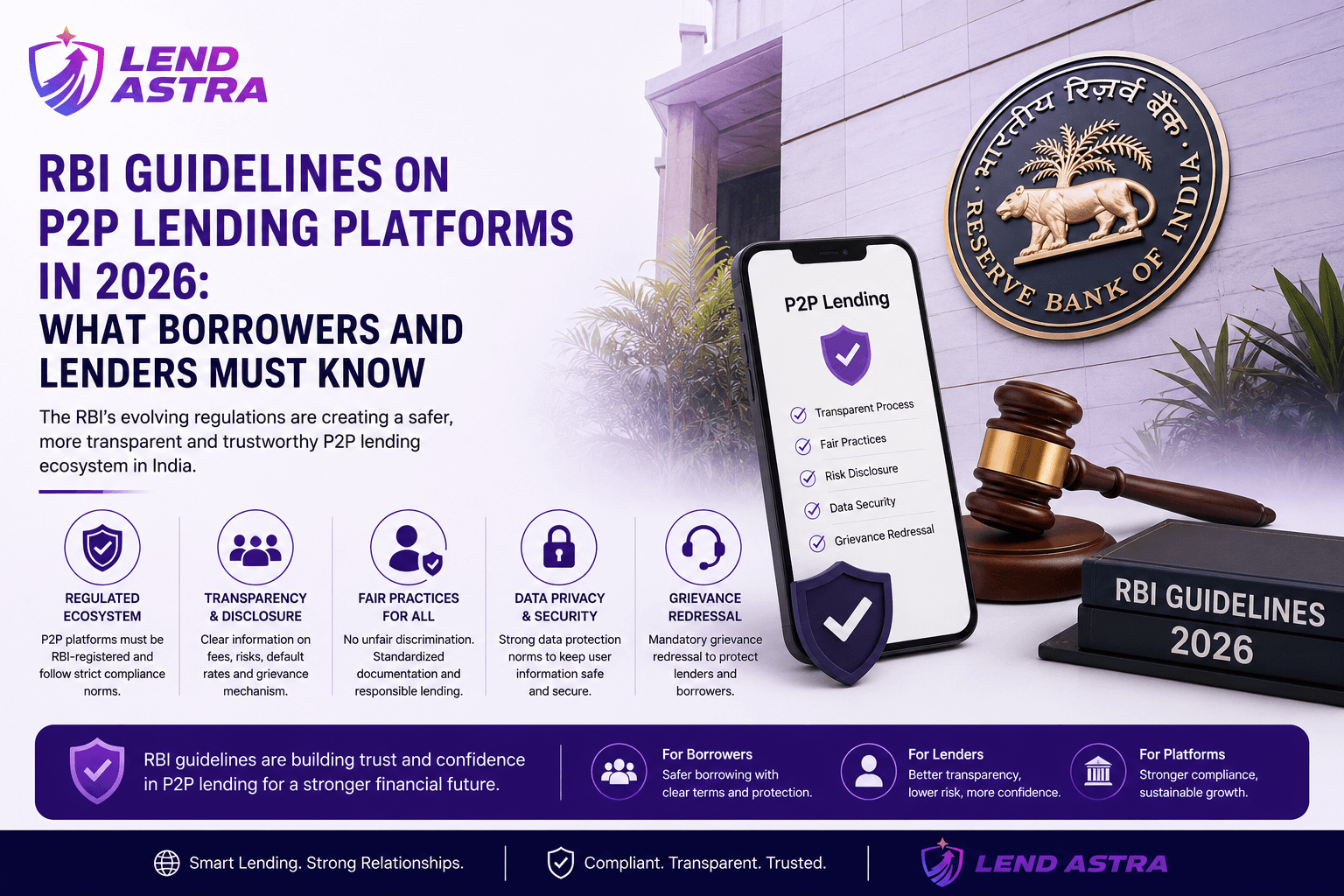

What "P2P lending" means under RBI rules

The RBI's foundational document here is the NBFC – Peer to Peer Lending Platform (Reserve Bank) Directions, 2017 (commonly called the "P2P Master Direction"), with successive amendments through 2024 and 2026.

A "P2P platform" under this framework is a company registered as NBFC-P2P with the RBI that acts as an intermediary between unrelated lenders and borrowers. Key characteristics:

- It's a registered NBFC (₹2 crore minimum net-owned funds requirement).

- It facilitates the loan, it does not lend off its own balance sheet.

- It collects, holds, and disburses funds via an escrow operated by a SEBI-registered trustee.

- It charges a service fee, not interest.

Examples of currently registered NBFC-P2P platforms (Faircent, LenDenClub, etc.). All have RBI registration certificates that are publicly listed at rbi.org.in.

The hard caps every P2P participant must know

| Cap | Limit |

|---|---|

| Maximum aggregate exposure of one lender across all NBFC-P2P platforms | ₹50,00,000 |

| Maximum aggregate exposure of one lender to one borrower | ₹50,000 |

| Maximum borrowing of one borrower across all NBFC-P2P platforms | ₹10,00,000 |

| Maximum loan tenure | 36 months |

| Funds idle in escrow | Must be deployed or returned within T+1 |

These caps exist for one reason: to prevent retail savers from accidentally building unsecured-debt portfolios that exceed what they can absorb if defaults rise.

What NBFC-P2P platforms cannot do

The RBI explicitly prohibits NBFC-P2Ps from:

- Lending off their own balance sheet.

- Providing or arranging credit guarantees / first-loss default cover.

- Cross-selling products other than insurance directly related to the loan.

- Holding funds outside the escrow.

- Using gamification / leaderboards to push lenders into riskier loans.

- Lending to / borrowing from the same individual on both sides.

The 2024 amendment tightened these substantially after a wave of unauthorised first-loss-guarantee schemes earlier that year.

Where does friend-to-friend lending sit in this framework?

Outside it.

When you lend ₹2 lakh to your cousin in Kharghar with a stamped loan agreement, you are not a P2P platform, and neither is the platform that generated the agreement template for you. The RBI's P2P Master Direction applies to registered NBFC intermediaries facilitating loans between strangers. A documented loan between two named individuals, with no intermediary acting as escrow + matchmaker, is governed by:

- The Indian Contract Act, 1872 (the agreement)

- The Negotiable Instruments Act, 1881 (if there's a promissory note)

- The Income Tax Act, 1961 (Sections 269SS, 269T, 194A, etc.)

- The relevant state Money-Lending Act (only if you lend as a business)

The ₹50,000 single-borrower lender cap does not apply to you. You can legally lend your sister ₹15 lakh on a written, stamped agreement.

When does private lending start needing a money-lender's licence?

The threshold isn't about a specific number, it's about frequency and purpose. State Money-Lending Acts (Maharashtra's 2014 statute, the Bombay 1946 Act for Mumbai city, the TN Money Lenders Act for Tamil Nadu, and so on) apply when you lend as a business or trade. Tests courts apply:

- Do you lend regularly to multiple unrelated borrowers?

- Do you charge interest at commercial rates?

- Do you advertise or solicit borrowers?

- Is lending one of your sources of livelihood?

Lending five times in a year to three different colleagues' relatives? Probably needs a licence. Lending once a year to your brother-in-law? Doesn't.

RBI's 2026 directions on digital lending, what changed

The Digital Lending Guidelines (introduced 2022, expanded 2024, refined 2026) sit alongside the P2P Master Direction and apply to any digital lending, including some private-lending platforms that handle disbursal. Key 2026 requirements:

- Loan disclosure key fact statement (KFS) must be provided in standardised format before disbursal.

- APR computation must follow the prescribed methodology, flat-interest claims that misrepresent effective APR are now violations.

- Cooling-off period of 1 working day for digital loans, during which the borrower can return the principal without penalty.

- Recovery agent KYC, even on outsourced collection, the platform is responsible for verifying agent identity and registering them.

- Grievance redressal mechanism with a published Nodal Officer.

A documentation-and-tracking platform like LendAstra that doesn't disburse or facilitate disbursal on behalf of strangers is generally outside the digital-lending guidelines' scope, but the platform's recovery and dispute features should still align with the principles (transparent KFS-equivalent, no harassment in recovery, etc.).

Practical implications for the average Indian lender in 2026

If you're lending to a known individual (family, colleague, friend):

- ✅ You can lend any amount on a documented agreement.

- ✅ No RBI registration needed.

- ✅ Income Tax Sections 269SS / 269T apply (₹20,000 cash limit).

- ✅ State stamp duty applies.

- ❌ No RBI grievance redressal, you go through civil courts.

If you're lending to strangers through a platform that matches you with borrowers:

- ✅ Only use RBI-registered NBFC-P2P platforms (verify via rbi.org.in).

- ✅ Lender cap: ₹50 lakh aggregate, ₹50,000 per borrower.

- ✅ Borrower cap: ₹10 lakh aggregate.

- ✅ Maximum tenure 36 months.

- ✅ RBI grievance redressal applies.

Two questions to ask before you click "Invest" on any P2P platform

- "Show me your RBI registration certificate." Real platforms link this in their footer. If it's not findable, walk away.

- "What's the 90-day-past-due NPA rate on your loan book?" Registered platforms must disclose this. Anything above ~7% in 2026 is a yellow flag.

Documented, regulation-aware lending, whether through an RBI-registered platform or directly to someone you know, is the only kind of lending that holds up when something goes wrong. The framework exists to protect you; understanding which piece of it applies to your situation is the first step.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3EMediation%20Over%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELitigation%3A%20Resolving%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELoan%20Disputes%20Without%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ENRI%20Lending%20to%20Family%20in%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EIndia%3A%20The%20FEMA%20Basics%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ERecovering%20a%20Loan%20Across%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStates%3A%20Jurisdiction%20and%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EWhere%20to%20File%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)