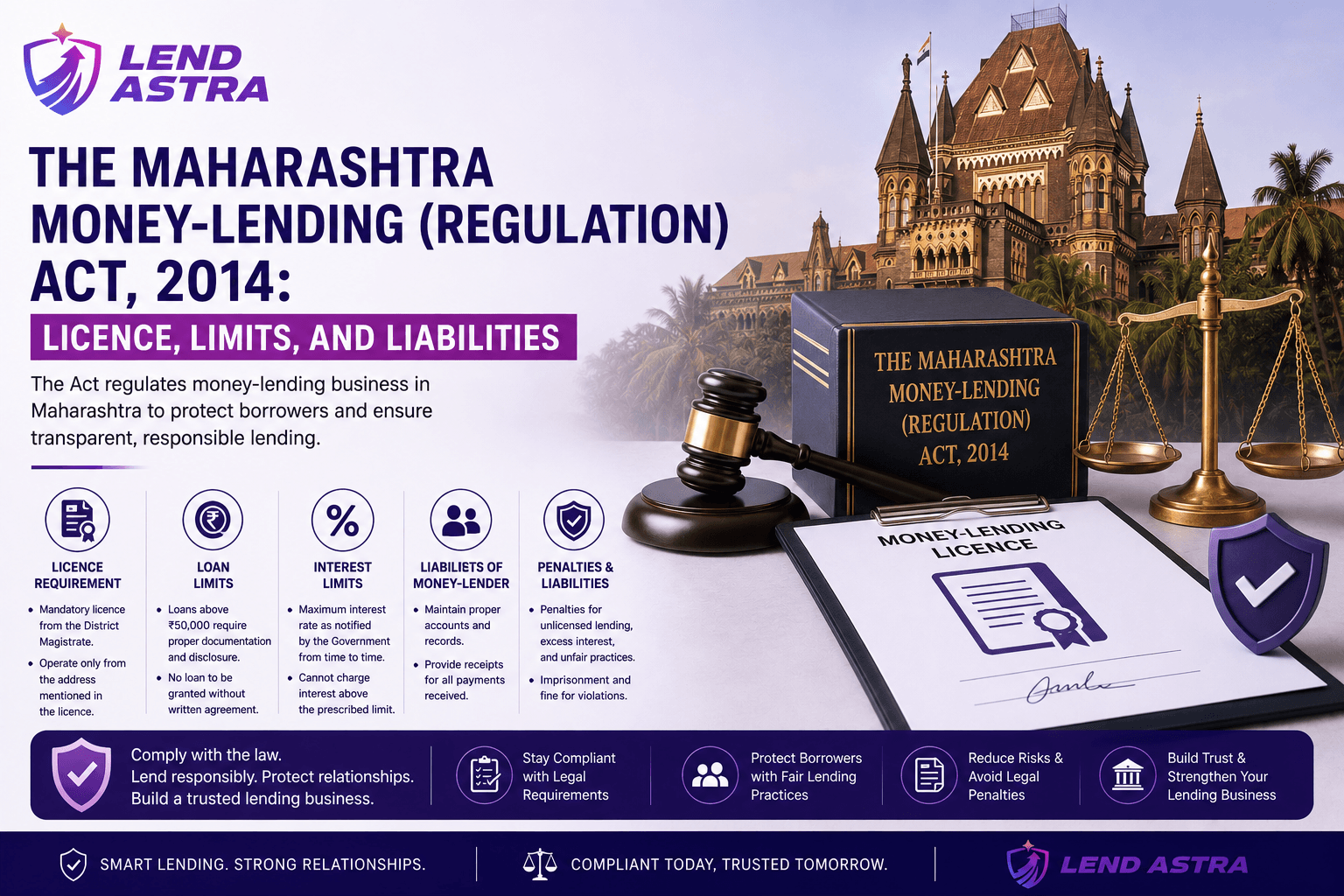

The Maharashtra Money-Lending (Regulation) Act, 2014 replaced the 68-year-old Bombay Money-Lenders Act, 1946, and tightened the regulatory net around anyone lending money as a trade or profession in the state. If you lend regularly, charge interest, and treat lending as a business activity, this Act is your operating manual.

It also defines, sharply, the line between personal lending (one-off, between known individuals) and professional money-lending (the regulated business). Knowing which side of that line you're on is the single most important thing if you lend in Maharashtra.

The core test: are you a "money-lender" under the Act?

Section 2(11) defines a money-lender as a person who:

"...carries on the business of money-lending in the State or has his principal place of such business in the State..."

Three operative phrases:

- "Business of money-lending", repeated, systematic, commercial activity. One loan to a brother-in-law is not a business; ten loans to ten different colleagues in a year is.

- "In the State", the lending activity occurs in Maharashtra, regardless of where the lender resides.

- "Principal place", even if some loans are made elsewhere, if your main lending operation is in Maharashtra, you're covered.

Courts apply a multi-factor test:

- Frequency. Multiple loans per year suggest business.

- Purpose. Lending to earn interest income vs lending as financial favour.

- Advertising. Soliciting borrowers (even via word-of-mouth networks) indicates business.

- Source of livelihood. Whether interest income forms a meaningful part of your income.

If three or more of these point to "business", you need a licence.

The licence application, what to expect

Applications are submitted to the District Deputy Registrar (DDR) of the district where you intend to lend. For Mumbai-region lenders, the relevant DDR offices are:

- Mumbai Suburban, Belapur (also handles Navi Mumbai)

- Mumbai City, Old Customs House, Fort

- Thane, Civil Lines, Thane West

- Raigad, Alibag

Documents required (2026):

- Application in Form A (prescribed under Maharashtra Money-Lending Rules, 2014)

- PAN, Aadhaar, photo of the applicant

- Address proof of principal place of business

- Proof of financial soundness (typically a bank balance certificate showing ≥ ₹50,000 net worth)

- Police clearance certificate (for the applicant, not older than 6 months)

- Proposed registered office address with rent receipt or ownership proof

- List of proposed places of lending business

- Application fee (currently ₹500–₹2,000 depending on lending volume tier)

The DDR conducts a verification, including a police background check, before issuing the licence. Total time: typically 60–120 days.

What a Maharashtra money-lender's licence permits and prohibits

Once you hold a valid licence:

Permitted:

- Lending money at interest within the state.

- Charging interest up to the state-prescribed ceiling.

- Operating from licensed places of business.

- Recovering loans through civil courts, including Order 37 CPC summary suits.

Prohibited (offences under the Act):

- Charging interest above the prescribed ceiling.

- Lending to a person under 18 years of age.

- Compounding interest more frequently than annually.

- Failing to maintain prescribed registers.

- Failing to issue receipts for every repayment.

- Operating from unlicensed premises.

- Threatening, intimidating, or harassing borrowers (this is treated severely post-2024 amendments).

Interest rate ceilings (current as of 2026)

The state government notifies maximum interest rates from time to time. As of the 2025 notification:

| Loan type | Maximum simple interest |

|---|---|

| Secured loan | 15% per annum |

| Unsecured loan | 18% per annum |

These are the maximum, many licensed lenders charge less to remain competitive. Charging above these rates makes the loan partially unenforceable: a court will refund the excess to the borrower.

Daily / monthly rates that need conversion. A common scam is to quote "1% per month" without disclosing the annualised rate. 1% per month is 12% per annum simple or 12.68% per annum compound, within the cap. "2% per month" is 24% per annum, over the cap and partially unenforceable.

Recordkeeping requirements, the heart of compliance

Every licensed money-lender must maintain:

- Register of borrowers (Form B), name, address, date of loan, amount, interest rate, security (if any), repayment schedule.

- Receipt book (Form C), duplicate-copy receipt for every repayment; one copy to borrower, one retained.

- Cashbook, daily disbursals and recoveries.

- Annual statement of accounts, submitted to the DDR within 60 days of the end of each financial year.

Failure to maintain these is itself an offence, and in any dispute, the absence of records is treated as adverse to the lender.

Penalties under the 2014 Act

The 2014 Act significantly strengthened penalties compared to the 1946 statute:

| Offence | Penalty |

|---|---|

| Lending without licence | Imprisonment up to 2 years + fine up to ₹50,000 |

| Charging interest above the ceiling | Refund of excess + fine up to ₹25,000 |

| Failure to maintain records | Fine up to ₹10,000 per breach |

| Harassment / coercion in recovery | Imprisonment up to 5 years + fine up to ₹50,000 |

| Repeat offences | Doubling of penalties + licence revocation |

The 2024 amendment added immediate licence-suspension powers to the DDR for serious complaints, pending inquiry, a significant strengthening from the prior regime where suspension required a court order.

How the Act interacts with personal lending

This is the question that comes up most. Three scenarios:

Scenario A: You lend ₹2 lakh to your cousin once a year.

→ Not a money-lender under the Act. The Indian Contract Act and (if there's a pro note) the Negotiable Instruments Act govern your loan. No licence needed.

Scenario B: You lend to five different unrelated borrowers over 12 months, all in Maharashtra, charging interest.

→ Almost certainly a money-lender under the Act. Apply for a licence before the next loan.

Scenario C: You run a chit fund or kitty group in Navi Mumbai.

→ Governed by the Chit Funds Act, 1982, not the ML Act, but the ML Act may apply if interest-bearing loans are extended outside the chit structure.

When in doubt, a one-time consultation with a local commercial lawyer (typical fee in Navi Mumbai: ₹2,000–₹5,000) gives clarity and protects you from a future criminal-procedure surprise.

What "Professional Lender" means in modern lending platforms

Platforms like LendAstra explicitly recognise licensed professional money-lenders as a distinct user category. The platform tracks the lender's:

- ML licence number (e.g., "MH-ML-2020-0001")

- Issuing DDR office

- Licence expiry date

- Maximum loan amount permitted

- State-act applicable

- Interest rate cap applicable

This makes professional-tier lending more discoverable, more trustworthy, and (importantly) keeps the licensed lender compliant with the Act's recordkeeping requirements by maintaining a real-time digital register of borrowers.

Three things to verify before any loan from a "professional money-lender" in Maharashtra

- Ask for the licence certificate. A genuine licence has a registration number, issuing DDR office, validity period, and the lender's photo. Don't accept a verbal "I'm licensed".

- Verify the interest rate. If quoted as "X% per month", convert to annualised. If above 15% (secured) or 18% (unsecured), the excess is unenforceable.

- Demand receipts for every repayment. Form C duplicate receipts are mandatory. The absence of receipts is the strongest evidence in any future dispute.

The 2014 Act exists to give borrowers protection from predatory practices that thrived under the old 1946 regime. Engage with licensed lenders, and the framework works in your favour.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3EMediation%20Over%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELitigation%3A%20Resolving%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3ELoan%20Disputes%20Without%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ENRI%20Lending%20to%20Family%20in%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EIndia%3A%20The%20FEMA%20Basics%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3ERecovering%20a%20Loan%20Across%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EStates%3A%20Jurisdiction%20and%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EWhere%20to%20File%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)