Five minutes of due diligence before you part with ₹1 lakh saves you eighteen months of recovery effort if things go wrong. Most private lenders skip these checks because they feel awkward, we're family, I've known him for years, what's there to verify? The defaulters are often the ones closest to you. Familiarity is not the same as creditworthiness.

These are the five checks that, in our recovery-pattern analysis, would have prevented over 60% of the disputes we see.

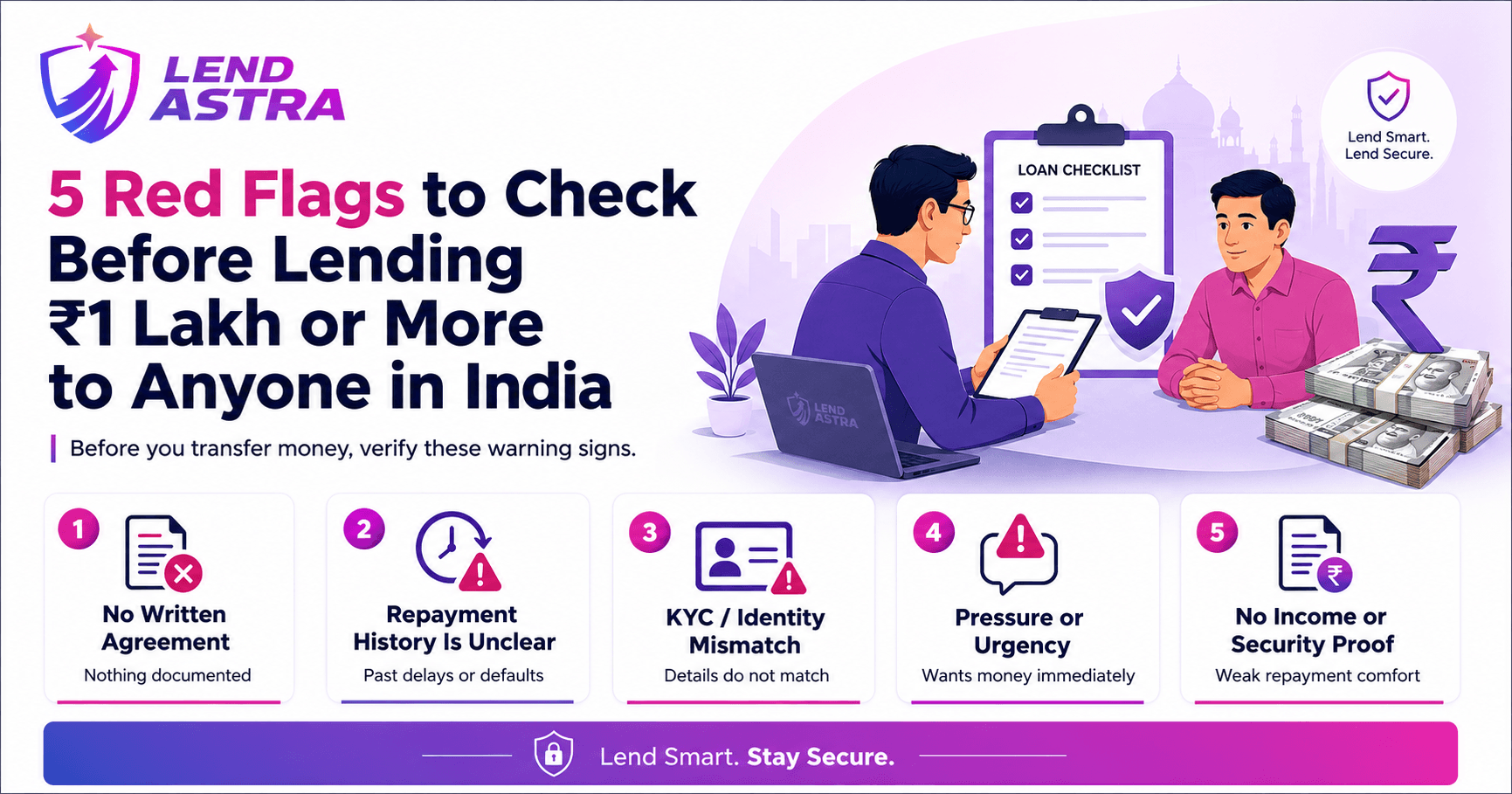

Red flag 1: They refuse to put it in writing

The single most predictive signal. If a borrower won't sign a one-page acknowledgment with the basic terms (amount, repayment date, mode of disbursal), they are either:

- Already mentally treating the money as a gift, or

- Anticipating they may not repay, and don't want a paper trail.

There is no third category.

What "refusal" looks like:

- "Let's just keep it informal, you trust me right?"

- "We don't need paperwork, that's not how family works."

- "I'll send you a WhatsApp message instead." (And then doesn't.)

- "We'll do it next week" (and never does).

- Anger or hurt feelings at the suggestion of documentation.

The reframe: "This isn't about trust, it's about clarity for both of us in six months. The same way we'd document a property sale even with the closest family." If they still refuse after that reframe, do not lend. You're protecting both the friendship and your money.

Red flag 2: Their CIBIL score is sub-650, or they refuse to share it

CIBIL (Credit Information Bureau India Ltd) maintains a credit history for every PAN-holder who has ever borrowed institutionally. The score ranges from 300 to 900:

| Score | Interpretation |

|---|---|

| 750–900 | Excellent, consistent repayment, low default risk |

| 700–749 | Good, minor issues, generally creditworthy |

| 650–699 | Fair, some late payments or limited history |

| 550–649 | Poor, multiple defaults or settlements |

| Below 550 | Very poor, significant default history |

Free check: Every Indian can pull their own CIBIL report once a year, free, at cibil.com. Score-only check costs ₹0; full report (with all loan accounts) costs ~₹550.

Ask: "Can you share your latest CIBIL score with me?" A creditworthy borrower will share it within minutes. A defaulter will hedge, change the subject, or claim "I don't have one" (which is itself a flag, anyone with a credit card or any loan has a CIBIL score).

Edge case: First-time borrowers (young professionals, recent migrants) may genuinely have no CIBIL history. In that case, request alternative proof: 6 months of bank statements, current employer letter, IT returns.

Red flag 3: The source of repayment is vague or implausible

Ask: "How are you planning to repay this?" Listen carefully to the answer.

Healthy answers:

- "I'll use my Diwali bonus in October."

- "I'm getting a TDS refund of ₹35,000 in September."

- "I get ₹40K/month after EMIs; I can comfortably set aside ₹15K from each salary."

- "I'm selling my Royal Enfield, expecting ₹1.2 lakh."

Yellow-flag answers:

- "Something will come up." (Hope is not a repayment plan.)

- "My uncle is going to give me money." (Borrowing-to-repay-borrowing is fragile.)

- "I have a side gig that should work out." (Unproven income.)

Red-flag answers:

- "I'll pay you back when I can." (No timeline = no plan.)

- "You don't need to worry about that." (Resistance to the question itself.)

- "I'm going to get a loan from another friend to repay you." (Active Ponzi behaviour.)

- "Some investment I made will pay off." (Especially if vague about what investment.)

A creditworthy borrower has a specific, plausible, time-bound repayment source. A defaulter has aspirations.

Red flag 4: The amount is meaningfully more than their declared income justifies

A rough rule of thumb in Indian personal-lending circles: any personal loan above 6× the borrower's monthly take-home salary is in elevated-risk territory. Above 12× is high-risk regardless of other factors.

Examples:

| Monthly take-home | Loan size at 6× | Loan size at 12× |

|---|---|---|

| ₹40,000 | ₹2,40,000 (acceptable) | ₹4,80,000 (elevated) |

| ₹75,000 | ₹4,50,000 (acceptable) | ₹9,00,000 (elevated) |

| ₹1,50,000 | ₹9,00,000 (acceptable) | ₹18,00,000 (elevated) |

This isn't a hard rule, it's a risk signal. A borrower with a windfall coming (property sale, bonus, parental contribution) can responsibly take on more than 6×. But ask the question: what makes this loan repayable from this income?

Verification methods:

- Latest 3 months of bank statements (look at salary credits)

- Latest Form 16 (annual taxable income from employer)

- ITR-V acknowledgment of last filed return

Red flag 5: They're already borrowing from multiple sources

Quietly check: how many other people are they currently in debt to?

Signals of multi-source borrowing:

- Multiple WhatsApp groups or social-media posts about needing money.

- Multiple recent UPI receipts from unrelated individuals (visible if you ask for bank statements).

- Multiple recent personal loans on their CIBIL report (visible in the full report).

- They've borrowed from you, repaid quickly, then asked for more, a classic "build trust then borrow big" pattern.

- They mention "I'm just consolidating my debts", almost always means they're underwater.

The single biggest predictor of default isn't the size of the loan, it's the number of concurrent creditors. A borrower juggling three personal loans + two credit cards + family debt has fragile cash flow that breaks the moment any one income stream disrupts.

A 10-minute due diligence checklist

Before you lend ₹1 lakh+:

- Verify PAN, quick check at incometaxindia.gov.in's "Verify PAN" tool (1 minute).

- Aadhaar / address proof copy, match against current residence.

- Latest CIBIL score, ask them to share theirs; or pull yours and theirs combined via authorised platforms (5 minutes).

- Last 3 months bank statement, for income verification and existing-debt visibility (1 minute to scan).

- Current employer letter (if salaried), or last ITR if self-employed (1 minute).

- Specific repayment plan, written, with dates (2 minutes of conversation).

If all five check out, your default risk drops by an order of magnitude. If even two raise flags, either reduce the loan amount, add collateral, or politely decline.

"Adding collateral", what works between individuals

For higher-risk borrowers you still want to help, ask for security:

- Post-dated cheques for each instalment. Bouncing one triggers Section 138 NI Act criminal proceedings.

- Gold pledge, held by the lender or in a sealed envelope with a third party, returned on full repayment. Common in Marathi and Gujarati lending traditions.

- Vehicle papers, held by the lender, returned on full repayment. Lower-friction than gold.

- Guarantor signature, a third creditworthy adult who co-signs and is jointly liable.

Collateral doesn't eliminate the conversation about red flags, it just changes the recovery economics. If the borrower is willing to put up collateral, they're at least confident enough in repayment to risk their own asset.

What to do if you've already disbursed and now see red flags

- Document immediately. Send a WhatsApp message that confirms the loan: "Hey, just to put on record. I transferred ₹3 lakh to you on 5 May, agreement is to repay by 5 November." Their response (whatever it is) becomes evidence.

- Start the repayment habit early. Don't wait for the full repayment date, request a small partial payment 30–60 days in. The way they respond to the first request tells you almost everything about how the full repayment will go.

- Tighten the friendship, don't loosen it. Counter-intuitively, the borrower's avoidance behaviour worsens the closer you get to default. Stay in regular friendly contact. Don't let the loan become the only topic; that's when conversations break down.

- Move toward formal documentation if you haven't. A late-stage acknowledgment letter, signed and dated today, is far better than no document, and resets the Limitation Act clock under Section 18.

The honest truth about lending to people you know

The data is unambiguous: about 30% of friend-loans in India fall into some form of dispute. Of those, about half result in damaged relationships even after the money is eventually recovered. Five minutes of pre-loan due diligence, these five red flags + a properly documented agreement, moves the relationship-damage probability from 15% to under 3%.

The five minutes are cheap. The eighteen months of awkward WhatsApp messages are not.

%22%2F%3E%3Ctext%20x%3D%2264%22%20y%3D%22140%22%20fill%3D%22%23EFB33D%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2226%22%20font-weight%3D%22700%22%20letter-spacing%3D%224%22%3ELEND%20ASTRA%3C%2Ftext%3E%3Ctext%20x%3D%2264%22%20y%3D%22300%22%20fill%3D%22%23F5F1E8%22%20font-family%3D%22system-ui%2CSegoe%20UI%2CArial%2Csans-serif%22%20font-size%3D%2250%22%20font-weight%3D%22800%22%3E%3Ctspan%20x%3D%2264%22%20dy%3D%220%22%3EThe%20Real%20Cost%20of%20an%3C%2Ftspan%3E%3Ctspan%20x%3D%2264%22%20dy%3D%2258%22%3EUndocumented%20Loan%3C%2Ftspan%3E%3C%2Ftext%3E%3C%2Fsvg%3E)